Well, no shrinking violet, our first female Chancellor Rachel Reeves delivered a very steely first Budget and we thought we would celebrate the Girl Power reminiscent of Labour’s last hey day in the 90s. Either that or we are just trying to relive our youth.

Anyway, in line with our favourite female pop group, we have picked our top five performers in the budget to give you a full run down, with some additional album tracks at the end to whet your appetite for a follow-up single.

So read on to find out whether we thought this year’s Budget was top totty or if it was a bit Scary Spice.

Stop right now!!

The Chancellor made a big deal this afternoon of reminding us how she was sticking to her manifesto pledges to ‘working people’, however they are defined. What has become clear is that any manifesto pledges certainly did not apply to the employers of those working people, who might be thinking the latest announcements are Mamadness!

defined. What has become clear is that any manifesto pledges certainly did not apply to the employers of those working people, who might be thinking the latest announcements are Mamadness!

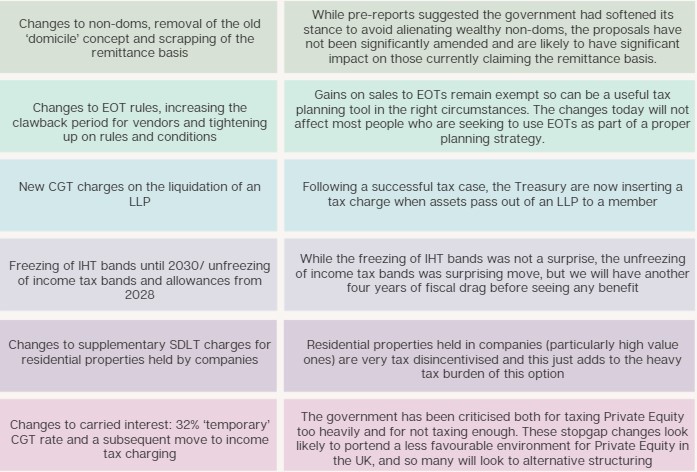

As with many Budgets of recent years, we have had leaks and rumours of changes, many of which turned out to be true. However, in some cases, it seems the leak has been to soften us up to the idea of a bigger rise than has actually been announced in the hope that it might be received more favourably. In addition to the early announcement of the increase in the National Minimum/Living Wage rates from April 2025, Ms Reeves confirmed two much-speculated changes to employer’s NIC, which will hit employers hard in terms of the additional cost of employing all those lovely working people she is seeking to protect.

Firstly, the rate of NIC will increase from 13.8% to 15% from 6 April 2025, a mere 1.2% rise instead of the pre-tested 2% (although that is really an 8.7% increase in the cost). The increase will also apply to the rate of Class 1A NIC payable on benefits provided to employees via the P11D process and Class 1B NIC payable on ‘minor’ benefits via a PAYE Settlement Agreement (PSA).

Secondly, the threshold at which the employer’s NIC becomes payable will be reduced to £5,000 from £9,100, fixed for the period 6 April 2025 to 5 April 2028, after which it will be increased in line with the Consumer Price Index (CPI).

So what does this mean for an employer who say employs 100 people at the National Living Wage rate working 40 hours per week. With the increase in NIC on a higher rate of pay and reduction in the threshold (and including the £10,500 Employment Allowance which will now apply to all employers), it will cost the employer an additional £85,000 per year (plus any additional Class 1A/B NIC) following today’s announcements! Of course, that extra cost will be deductible for corporation tax purposes but that is cold comfort and it certainly sounds like something kinda funny going on there.

On a more positive note, the chancellor announced an increase in the Employment Allowance (EA) from £5,000 to £10,500 from 6 April 2025. She also announced the removal of the restriction where employers could not claim the allowance if their total employers’ was more than £100,000 in the previous tax year, which means that all employers should be able to claim (subject to meeting certain conditions). Finally, there is no suggestion that employer contributions to employees pension schemes would become subject to NI, presumably because that would likely have ended up impacting the working people…

I really really really wanna crystallise a gain

Much of the pre-Budget hysteria has centred on the possible increases to capital gains tax (CGT) rates, with much speculation that would rise from the existing 10%/20% rates on standard gains up to rates somewhere in the 30-40% range. Who’d wannabe an entrepreneur in the UK huh?

Much of the pre-Budget hysteria has centred on the possible increases to capital gains tax (CGT) rates, with much speculation that would rise from the existing 10%/20% rates on standard gains up to rates somewhere in the 30-40% range. Who’d wannabe an entrepreneur in the UK huh?

In the end, CGT rates have been increased but perhaps not by as much as people had feared. But are the increases still too much?

While many things in tax are complicated, in fact the changes are not so difficult. For gains falling within the basic rate of income tax, the rate is rising from 10% to 18%, and for all other gains (excluding those subject to special rates or other reliefs, see below), the rate is increasing from 20% to 24%.This aligns with the rates of tax on residential property gains, such that all assets (with the exception of carried interest) are now taxable at the same rates.

The rates apply from budget day, so 30 October 2024, and there are a raft of anti-forestalling measures that will be included in the Finance Bill to prevent individuals seeking to hedge their bets by leaving deals resting on unconditional contracts, for example, or certain arrangements involving company reconstructions. This, of course, means that the announcements currently have the force of law, and when (assuming) the Finance Bill receives Royal Assent, these changes will be backdated to today. While annoying, those who did rush to complete a transaction may be patting themselves on the back having saved a whopping 4% in tax (let’s hope any deal acceleration was worth it!), but overall the consensus seems to be that this raise was not as bad as was feared.

Business Asset Disposal Relief (BADR) also lives to fight another day. The current 10% rate that applies to gains will also be aligned with the lower rate of CGT, although there is at least some tapering in of the rate. The 10% rate will apply for disposals up to 5 April 2025, with a transitional 14% rate applying until 5 April 2026, and gains attracting the 18% rate thereafter. Given the £1m lifetime limit still applies and the narrowing of the gap between the higher and lower rates of CGT this means that from 2026 onwards, the maximum benefit of BADR will be £60,000. Possibly not enough to spice up your life. It also seemed disingenuous of the Chancellor to present the retention of the £1m lifetime allowance as an act of generosity given the previous limit of £10m.

Talking of lifetime limits, Investor’s Relief is often overlooked, and some might say it has only maintained its £10m limit for the past four years because someone in the Treasury forgot about it. Nevertheless, it is now subject to a £1m limit from 30 October 2024 (10 becomes 1 perhaps?), and with the same tapering up of the rate from 10% to 18% as for BADR. Similar anti-forestalling rules will also apply, and for the purposes of a s169VT election (similar to the s169Q election for BADR which crystallises a gain on a share for share exchange which would otherwise be tax free), even though individuals may still make an election in respect of gains crystallised prior to the change, the limit in force will be the £10m or £1m at the time of making the election, just in case you had any bright ideas.

So is this tax rise the oft-portended end for entrepreneurship in the UK? Unlikely. A 4% increase in tax while not welcomed, is certainly better than many had feared and is still sufficiently lower than income tax for entrepreneurs to feel not so hard done by. What may happen, though, is we see increased activity at the smaller end of the market as those looking to cash in on their 10% BADR aim to do so before the end of the tax year.

Bye Bye BPR

Bye Bye BPR

They say good things must come to an end and it looks like we are going to have to say Goodbye to the good times with those most valuable of inheritance tax (IHT) reliefs, Agricultural Property Relief (APR) and Business Property Relief (BPR). While we may have wanted these reliefs to Viva Forever, even if both death and taxes are a certainty, the end of the road is approaching in a Thelma and Louise Style cliff edge.

Of course, as with anything IHT related, being able to plan the exact date of your own death is key, and if you manage to pop your clogs before 6th April 2026 you won’t be caught by the changes. However, for those of us looking slightly further towards the future, the prospect of the changes are daunting. As a reminder, the APR and BPR rules were introduced to prevent the need to break up or sell a family business or farm in order to fund the IHT liability arising on death. Now, it seems, preserving family business or farming interests is only of paramount importance for those holding assets of £1m or less, as any excess assets qualifying over a combined £1m total will only attract relief at 50%. Similarly, AIM shareholdings will now only get BPR at 50% from now on. But it’s fine, says the Treasury’s policy paper, you can pay the tax by instalments over ten years, with a hefty interest rate they have in the same breath increased by 1.5% to a current 9% per annum (compound).

So is there any way round this? The policy paper starts by saying that the rules apply from 6 April 2026 and that it applies to assets in a death estate. So far so good, and all you need to do is gift your assets away such that they aren’t in your death estate by then, right? Well kinda. The actual assets included will include failed PETs, potentially exempt transfers that only become exempt provided you survive seven years, but also all chargeable lifetime transfers (no time limit mentioned).

Does this mean then that any gifts into trust, the most common example of chargeable lifetime transfers, will also be included with no time limit? It appears so.

However, the new rules don’t come in until 2026, so you could just put all your shares into trust now, right? You’d think so. Unfortunately not. Anti-forestalling measures will bring into the new rules any lifetime gifts made after 30 October 2024 where the settlor (or donor) dies on or after 6 April 2026 having not survived seven years. So to reiterate, the only way to avoid the charge would be to expediate your demise.

It is worth noting, however, that when considering lifetime transfers of shares in private companies, valuation is an important factor. What is £1m of value? Typically, substantial discounts are applied to the value of private company shares for tax purposes to reflect their lack of saleability on the open market, and also to reflect lack of influence and control if it is a minority stake. Therefore, transferring shares into trust can still be very appealing prior to a sale process in the right circumstances. A shareholding subject to a hefty discount could be worth only £1m for tax purposes, but could be worth substantially more than that in the future when the shares are sold for cash.

But it isn’t all bad news, in a scraping of the bottom of the barrel kind of way, because the CGT uplift on death remains, such that at least on the first £1m, assets could be realised free of tax. You can also, as ever with IHT, gift APR or BPR assets away to individuals free of tax more than seven years before you die and still pay no IHT, which may be good for some businesses, particularly those still ruled by an ageing ogre who likes things done a certain way (Oh, hello Iain!).

Finally, it is worth noting that the £1m allowance applies per person, so any business owner who is married or in a civil partnership could conceivably transfer £1m worth of shares to their other half by spouse exemption, with the couple then creating two trusts, thereby doubling the IHT protection (though post-transfer said other half would be under no obligation to subsequently transfer those shares into trust, so a fair amount of, trust, is needed in more than one respect).

Transfer pricing

Those who watched the Budget announcement live today will probably have noticed that some statements garnered stronger responses than others – whether those were cheers or jeers – and the Chancellor certainly seemed to be embracing the Christmas spirit early with a panto style delivery of the decision to continue the 5p cut to fuel duty (for now). Rachel Reeves must have been thinking about Christmas Wrapping (talk about deep cuts!).

– whether those were cheers or jeers – and the Chancellor certainly seemed to be embracing the Christmas spirit early with a panto style delivery of the decision to continue the 5p cut to fuel duty (for now). Rachel Reeves must have been thinking about Christmas Wrapping (talk about deep cuts!).

There’s no Denying, slightly less likely to grab the headlines than “A penny off the pint in the pub” is the news that there will be a technical consultation on draft legislation to modernise and simplify three elements of UK tax legislation (being transfer pricing, permanent establishments and Diverted Profits Tax (DPT).

However, new proposals announced today include plans to bring medium sized businesses into the scope of transfer pricing regulations, the introduction of a new filing obligation for transactions, and revising transfer pricing treatment of cost contribution arrangements with a view to encouraging inward investment and development of intellectual property. Currently SMEs are generally not included within the scope of transfer pricing legislation, but the proposal would draw medium businesses (those with no more than 250 employees and either (a) no more than €50m turnover or (b) balance sheet total no more than €43m), into the transfer pricing net but small businesses (those with no more than 50 employees and either (a) no more than €10m turnover or (b) balance sheet total no more than €10m) will still be able to live in blissful ignorance.

My crystal ball (and Mystic Meg wig, for those old enough to remember contemporaries of the Spice Girls) will remain locked away in my drawer for now, but certainly it doesn’t seem a stretch to consider the possibility of many medium sized businesses that never previously needed to consider transfer pricing arrangements being in the position of needing to consider their arrangements and submit an informative return. Not quite Overnight, but it could be at short notice.

The consultation may lead to DPT becoming part of Corporation Tax, potentially allowing for double tax relief under treaty in the case of a DPT charge. This is not currently the case. So… Two Become One?

Over the past 18 months or so there has been legislation from HMRC on transfer pricing documentation for large businesses (those within the scope of country by country reporting) and practical guidance particularly helpful for smaller groups within the scope of the UK Transfer Pricing rules.

The practical guidance that came from HMRC earlier this year likely gave budget-constrained tax managers some comfort if they were unable to get professional advice. The current consultations could suggest that many more businesses are going to be in that position.

Throwing minimum global corporation tax rules into the mix means that many businesses are likely to feel they have a significant admin burden already and a web of incredibly complex rules to navigate, despite the fact they are often positioned as “simplifying” transfer pricing.

“I’m giving you everything”

Another area that saw much speculation in the pre-Budget hype concerned the taxation of pensions and more specifically, whether the 25%* tax-free lump sum would be limited or reduced, possibly down to £100k or less. However, given pensions were essentially an IHT free pot that could be passed down, prematurely taking out a pension lump sum might not have been the right advice and could, in fact, have resulted in a higher overall tax liability if the cash had not been spent before death.

In the end, the most anticipated change did not come about, and the 25%* tax free lump sum remains as it was, but instead, the pension fund itself will now fall back into IHT charge (at 40%) from 6 April 2027. Again, it seems the most tax efficient route would be to expire before the tax relief does.

While detail on the rules will not be included in the Finance Bill 2024, but will be prepared at some undefined later point, today’s announcement suggests that it will be the pension scheme administrator who will be required to deduct the tax due. Given the scheme will not have full details of the deceased’s estate, it feels, perhaps like this might end up being a tax credit that can be applied to the estate and a refund required if the tax deducted proves to be excessive. Presumably there would also be exemptions from charge if the pension was passing to a spouse, but we will have to await the detail.

While we don’t have the exact rules and cannot predict our deaths, this does mean that the way we advise clients might be slightly different. Previously, we would advise clients to spend down other pots of cash first, rather than touching a pension pot with its tax-favoured status. Now, with other IHT reliefs on death being severely curtailed, more nuanced planning will be necessary. Again, the constant messing about with pension rules does not necessarily enamour them as an investment vehicle, particularly once IHT benefits are lost, and clients might holler about how unfair it is to change the treatment of thousands of pounds invested under the knowledge of one tax treatment, only for that treatment to change have a retrospective effect on past investments.

* It is mostly 25%. If your pension fund exceeds £1,073,100 the maximum tax-free lump sum will be less than 25%, subject to any protections in place.

While we have gone not a little more detail in the five spices above, there were a number of other things announced today that might be of interest. Over the coming weeks we will dive a little deeper into these but for now, here is our track list…

All in all, we aren’t sure that the budget was the runaway hit the Chancellor would have liked, but perhaps putting the frighteners on us all beforehand made the actual delivery of her announcements a bit easier to swallow. That said, some of the changes will stick in the throats, particularly of employers and business owners and so if you fall into these camps you are likely to need a #1 tax adviser. All our lovely Claritas clients are saying that all they want from us is a promise to say we’ll be there… we will.